Personal Banking

Award-winning banking at your fingertips

Our rewarding LevelUp Checking account, interest-earning LevelUp Savings account, and competitive CDs will help you meet your goals.

LevelUp Savings

Earn 10x the National Average2

Get 4.00% APY on your balance when you deposit $250+ per month.3

Freedom from fees

Keep more of your money with no account fees and free transfers.

$0 minimum balance

No minimum to open or minimum balances required.

LevelUp Checking

LevelUp your money with our reward-earning checking account.

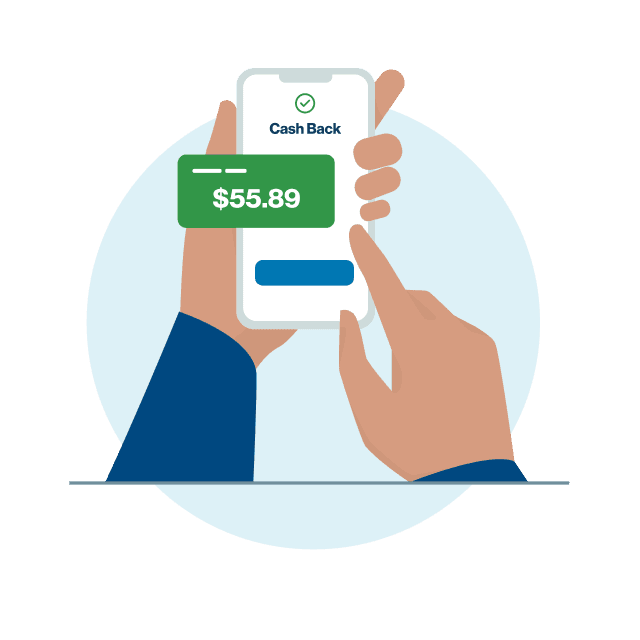

Cash Back Rewards

You could earn 1% cash back on debit card purchases and 2% cash back for on-time LendingClub personal loan payments with Direct Deposit.4, 5

Freedom from Fees

$0 minimum balances, no account fees, and free transfers. Also, enjoy unlimited ATM fee rebates!6

Get Paid Early

Set up direct deposit and you could get your paycheck up to 2 days earlier.7

Certificates of Deposit

6 Month Earn 3.90% APY8

8 Month Earn 4.15% APY8

1 Year Earn 3.50% APY8

18 Month Earn 3.50% APY8

2 Year Earn 3.50% APY8

5 Year Earn 3.40% APY8

Open a LevelUp account in minutes

Start earning more today. What are you waiting for?

Your reward-earning gets

better in the app

Make the smartest money move of the day.

Download the LendingClub app now.9

![]()

![]()

Security

FDIC Insurance

Customer support

Chat with us online, or reach us by phone or email.