What is a Personal Loan, How They Work and How to Apply

Key Takeaways

Personal loans can be used to pay for almost any type of expense.

You typically don’t need to put down any collateral to qualify, but most lenders review your credit history and other factors when you apply.

Personal loans are widely available from banks, credit unions, and online lenders, so it’s a good idea to shop around and compare rates.

Whether you need to replace a leaky roof, your wedding day is quickly approaching, or you want to consolidate high-interest debt, a personal loan can help provide a financial boost. Personal loans can offer competitive interest rates compared to credit cards and provide more flexibility than traditional mortgages or auto loans, depending on your individual credit profile and the terms of the loan. This article takes a closer look at how personal loans work and how to apply.

What is a Personal Loan and How Do They Work?

A personal loan is a type of installment loan that can be used for almost any purpose. People often take out a personal loan to help with debt consolidation or to cover a large one-time expense, like a wedding or home repairs. Personal loans are typically unsecured — meaning you don’t need to put down any collateral to qualify. You can apply for a personal loan at most banks and credit unions along with online lenders. Loan terms vary by lender, but you can typically expect flexible to moderate-term repayment options and quick funding.

Common Uses for Personal Loans

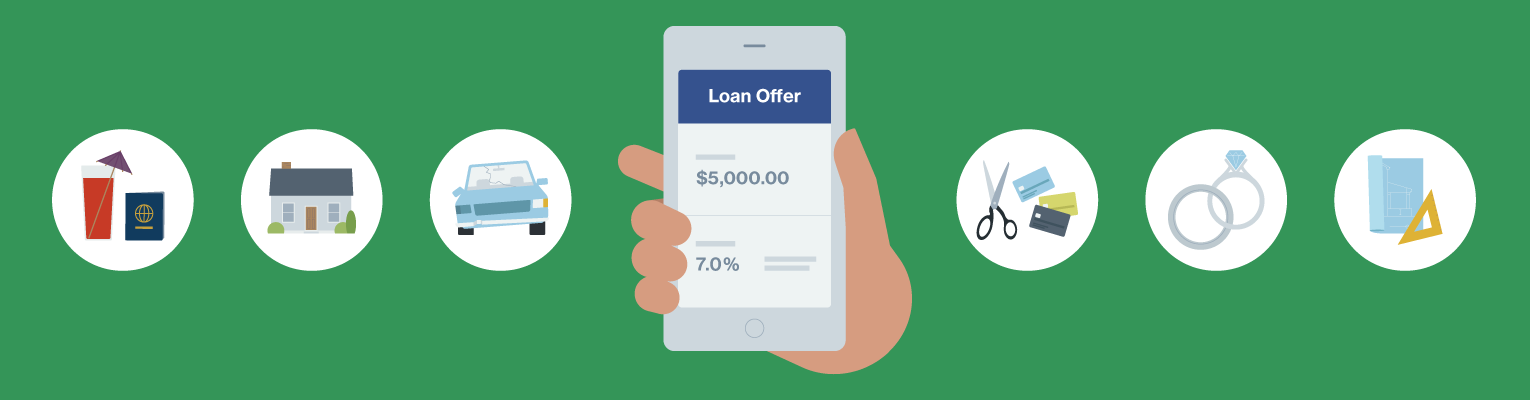

In general, personal loans can be used for almost any purpose except buying a house or paying for education. When shopping around for a personal loan, it’s important to double check that the lender doesn’t have any restrictions on how you plan to use the loan. Here’s a closer look at some common ways personal loans can be used:

Debt consolidation: A personal loan can help you consolidate your debt from multiple revolving credit cards with high (and often variable) interest rates into one manageable payment. Personal loans may offer lower interest rates compared to credit cards, depending on individual creditworthiness and loan terms.

Home renovation and repairs: Unlike a home equity loan or home equity line of credit (HELOC), a home improvement personal loan lets you avoid the risk of using your home as collateral for a loan to make needed repairs or improvements. You can use a personal loan for something minor (like replacing your water heater), something major (like finally upgrading those 1960s kitchen countertops), and pretty much everything in between.

Major purchases: High interest rates can rack up quickly on credit cards. Using them to make very large purchases that you may not be able to pay off within a month or two isn’t always the best financial move. With fixed and often competitive rates, personal loans can be used to make major purchases or pay for major life milestones, such as welcoming a new member of the family or hosting a wedding.

Paying back friends and family: Sometimes lingering loans from family and friends can make relationships a bit sticky. A personal loan can help you avoid the need to borrow from your inner circle or help you pay back an existing family loan.

Emergencies and urgent expenses: Even if you’ve been persistently building your emergency fund, a crisis can outstrip your nest egg. If your car breaks down, your pet gets sick, or your hot water heater needs to be replaced immediately, funds from a personal loan can help you handle the crisis and get back on track financially without having to dip into your savings account.

How Are Personal Loan Interest Rates and Terms Determined?

Personal loan interest rates and terms vary by lender and are based on several different factors. Lenders typically look at your creditworthiness to determine your interest rate. People with higher credit scores tend to qualify for better rates.

It’s possible to qualify for a personal loan with less-than-perfect credit since many lenders look at other factors such as your repayment history and debt-to-income ratio. Personal loan interest rates are typically fixed. It’s important to note that they’re also influenced by the federal funds rate set by the Federal Reserve (Fed).

Other loan terms, such as loan amount, loan length, repayment options, funding speed, and fees range widely between lenders. Most personal loans range from about $1,000 to $40,000, with loan lengths of roughly two to seven years. Lenders may also charge origination fees, late payment fees, or prepayment penalties. It’s a good idea to find a lender that charges as few fees as possible. For instance, LendingClub doesn’t charge a fee for paying off your loan early.

To get the cheapest loan rates, it’s important to compare offers from different lenders. For the most complete look at what you can expect to pay for the loan over time, take note of the loan’s annual percentage rate (APR), rather than its interest rate. APR includes the interest rate, plus any other charges and fees.

Common Pitfalls to Avoid if You’re Considering a Personal Loan

Before taking out a personal loan, it’s important to watch out for some common pitfalls, including:

Taking on extra debt you can’t afford. Using a personal loan to consolidate high-interest credit card debt into one payment can reduce your monthly debt obligations. But if you’re already strapped for cash and using a personal loan to pay for a big expense, it may be better to wait until you have more wiggle room in your budget.

Fees and other terms. Before you sign for a loan, it’s important to understand the fine print. This can help you avoid costly charges like late fees or prepayment fees.

High interest rates and less desirable terms. If your credit is less-than-perfect, you may only qualify for loans that cater to people who are improving their credit. Typically these loans have higher interest rates and low loan limits. If you’re able to wait to apply until you’ve had a chance to improve your credit, you may be able to qualify for a cheaper rate and better terms.

Follow These 3 Steps When Applying for a Personal Loan

If you’ve decided to apply for a personal loan, follow these steps to get the application process going:

1. Review your credit report

People with good credit generally qualify for the best personal loan rates. Before applying, it’s a good idea to check your credit score and double check your credit report to confirm there aren’t any errors. Free weekly credit reports are available from each of the three major bureaus (Equifax, TransUnion, and Experian). Credit scores are also available free from many banks, credit card issuers, and online services that match subscribers to credit offers.

2. Compare different loan options

To find the best rate and terms for your budget and needs, it’s important to compare rates and terms from different lenders, including APR, loan term, fees, loan amount, monthly payment, and lender reputation.

Before deciding to apply, consider rate shopping with lenders that offer pre-qualification without a hard credit check. LendingClub Bank, for example, uses a soft pull, equivalent to one recorded when you view your own credit score, to let you check rates without any impact to your score.

3. Complete your loan application and wait for funding

After deciding on a lender, it’s time to submit your official application. Typically you can expect to submit documentation such as a photo ID, recent utility bills, or pay stub to verify personal information like your identity, income, and where you live. Once you’ve submitted the application, the lender reviews your documentation and typically performs a hard credit check. If your loan is approved, be sure to review the fine print before accepting the offer, as rates and terms can change between prequalification and a final loan offer.

The Bottom Line

A personal loan can come in handy to help you consolidate high-interest debt or pay for a large purchase or an unexpected expense. Rates and terms vary widely by lender and may be affected by your credit history. Be sure to compare options from different banks, credit unions, and online lenders to find a personal loan that fits your financial situation best. But if you’re unable to qualify for the terms you want, consider taking steps to improve your credit or reapplying with a co-borrower.

You May Also Like